Amount of non-performing loans in the construction sector grew in August

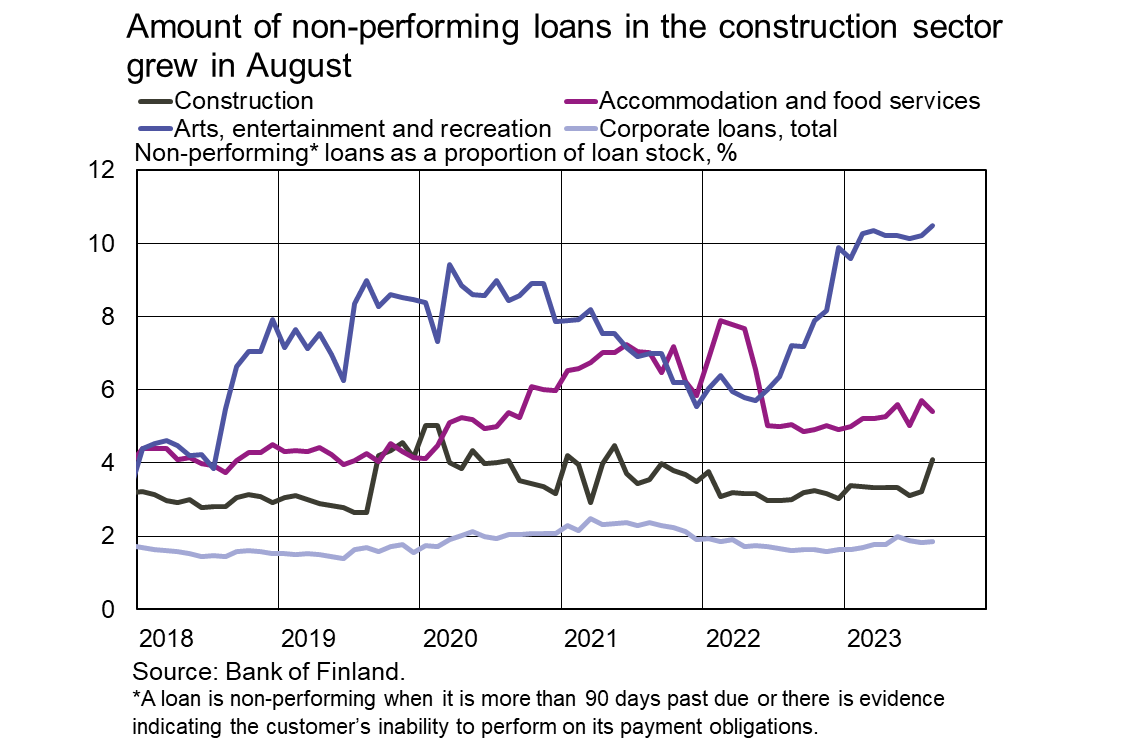

At the end of August 2023, a total of 4.1% of the stock of loans granted to Finnish companies in the construction sector was classified as non-performing. The share of non-performing loans rose by 0.9 percentage points from July. In August 2023, non-performing loans accounted for 1.9% of the entire corporate loan stock (EUR 62.0 billion). Impairments and credit losses recognised on loans granted to companies in the construction sector have also increased this year.

At the end of August 2023, a total of 4.1%, or EUR 123 million, of the stock of loans granted to Finnish companies in the construction sector was classified as non-performing[1]. The share of non-performing loans rose by 0.9 percentage points (EUR 26 million) from July. In August, sectors with higher shares of non-performing loans than construction were entertainment[2] (10.5%), health and social services (7.2%) as well as accommodation and food service (5.4%)[3].

Overall, the volume of non-performing corporate loans[4] has increased slightly from last year, while still remaining low as a proportion of the entire corporate loan stock. In August 2023, non-performing loans accounted for 1.9% of the corporate loan stock (EUR 62.0 billion), as opposed to 1.6% in last year’s August (out of EUR 64.5 billion).

Impairments[5] and credit losses recognised on loans granted to companies in the construction sector have also increased this year, while impairments and credit losses on corporate loans as a whole have stayed at a low level. In the past 12 months, Finnish credit institutions have booked a total of EUR 134 million of impairments and credit losses on corporate loans (0.22% of the August 2023 corporate loan stock). During these 12 months, the highest proportion of impairments and credit losses were booked on loans granted to companies in the construction sector (2.26% of the stock in August 2023). In other sectors, this ratio was clearly lower than in the construction sector (below 1% in the highest case). However, even in the construction sector, proportional impairments and credit losses still remain clearly lower than in 2020, when the ratio exceeded 3%.

Loans

In August 2023, Finnish households drew down EUR 1.1 billion of new housing loans, which is EUR 340 million less than in the same period a year earlier. Buy-to-let mortgage loans accounted for EUR 110 million of the new housing loan drawdowns. The average interest rate on new housing loans remained unchanged from July, to stand at 4.55% in August. At the end of August 2023, the housing loan stock totalled EUR 106.7 billion, and its year-on-year growth rate was -1.6%. Buy-to-let mortgage loans accounted for EUR 8.6 billion of the housing loan stock. At the end of August, the Finnish household loan stock included EUR 17.2 billion of consumer credit and EUR 17.8 billion of other loans.

Drawdowns of new loans by Finnish non-financial corporations in August totalled EUR 1.5 billion, including EUR 400 million of loans to housing corporations . The average interest rate on new corporate-loan drawdowns rose from July, to stand at 5.57 %. At the end of August, the stock of loans granted to Finnish non-financial corporations was EUR 105.4 billion, whereof housing corporations accounted for EUR 43.4 billion.

Deposits

At the end of August 2023, the stock of Finnish households’ deposits totalled EUR 109.3 billion, and the average interest rate on these deposits was 0.85%. Overnight deposits accounted for EUR 75.1 billion and deposits with an agreed maturity for EUR 8.3 billion of the total deposit stock. In August, Finnish households made new agreements on deposits with an agreed maturity in the amount of EUR 880 million, The average interest rate on new deposits with an agreed maturity was 2.97% in August.

| Loans and deposits to Finland, preliminary data* | |||||

| June, EUR million | July, EUR million | August, EUR million | August, 12-month change1, % | Average interest rate, % | |

| Loans to households, stock | 141,896 | 141,675 | 141,676 | -1.3 | 4.28 |

| - of which housing loans | 107,092 | 106,855 | 106,749 | -1.6 | 3.73 |

| - of which buy-to-let mortgages | 8,638 | 8,622 | 8,640 | 3.92 | |

| Loans to non-financial corporations2, stock | 105,688 | 105,263 | 105,407 | -0.1 | 4.44 |

| Deposits by households, stock | 110,877 | 109,878 | 109,278 | -3.4 | 0.85 |

| Households' new drawdowns of housing loans | 1,313 | 1,005 | 1,139 | 4.55 | |

| - of which buy-to-let mortgages | 106 | 86 | 112 | 4.73 | |

* Includes loans and deposits in all currencies to residents in Finland. The statistical releases of the Bank of Finland up to January 2021, as well as those of the ECB, present loans and deposits in euro to euro area residents and also include non-profit institutions serving households. For these reasons, the figures in this table differ from those in the aforementioned releases.

1 Rate of change has been calculated from monthly differences in levels adjusted for classification and other revaluation changes.

2 Non-financial corporations also include housing corporations.

- Euro-denominated deposits and loans of euro area residents: stock, 12 month rate of change and average interest rate

- Euro-denominated loans and deposits of Finnish households

- New business on loans and new drawdowns of household loans

- Finnish contribution to the euro area monetary aggregates and their main counterparts

- Imputed interest rate margins on loans from MFIs

For further information, please contact:

Antti Hirvonen, tel. +358 9 183 2121, email: antti.hirvonen(at)bof.fi,

Usva Topo, tel. +358 9 183 2056, email: usva.topo(at)bof.fi.

The next news release on money and banking statistics will be published at 10:00 on 31 October 2023.

Related statistical data and graphs are also available on the Bank of Finland website: . https://www.suomenpankki.fi/en/statistics2/.

[1] A loan is defined non-performing when a receivable is more than 90 days past due or there is evidence indicating the customer's inability to perform on its payment obligations.

[2] The arts, entertainment and recreation sector.

[3] In August 2023, out of the entire corporate loan stock (EUR 62.0 billion, excl. housing corporations), loans granted to the construction sector accounted for EUR 3.0 billion, the accommodation and food service sector for EUR 785 million, the health and social services sector for EUR 775 million and the arts, entertainment and recreation sector for EUR 467 million.

[4] Excl. housing corporations.

[5] Impairments are recognised on loans based on expected credit loss models. Expected credit loss is the bank’s assessment of the amount of credit that will not be repaid by the customer.