Housing loan stock contracted from a year ago

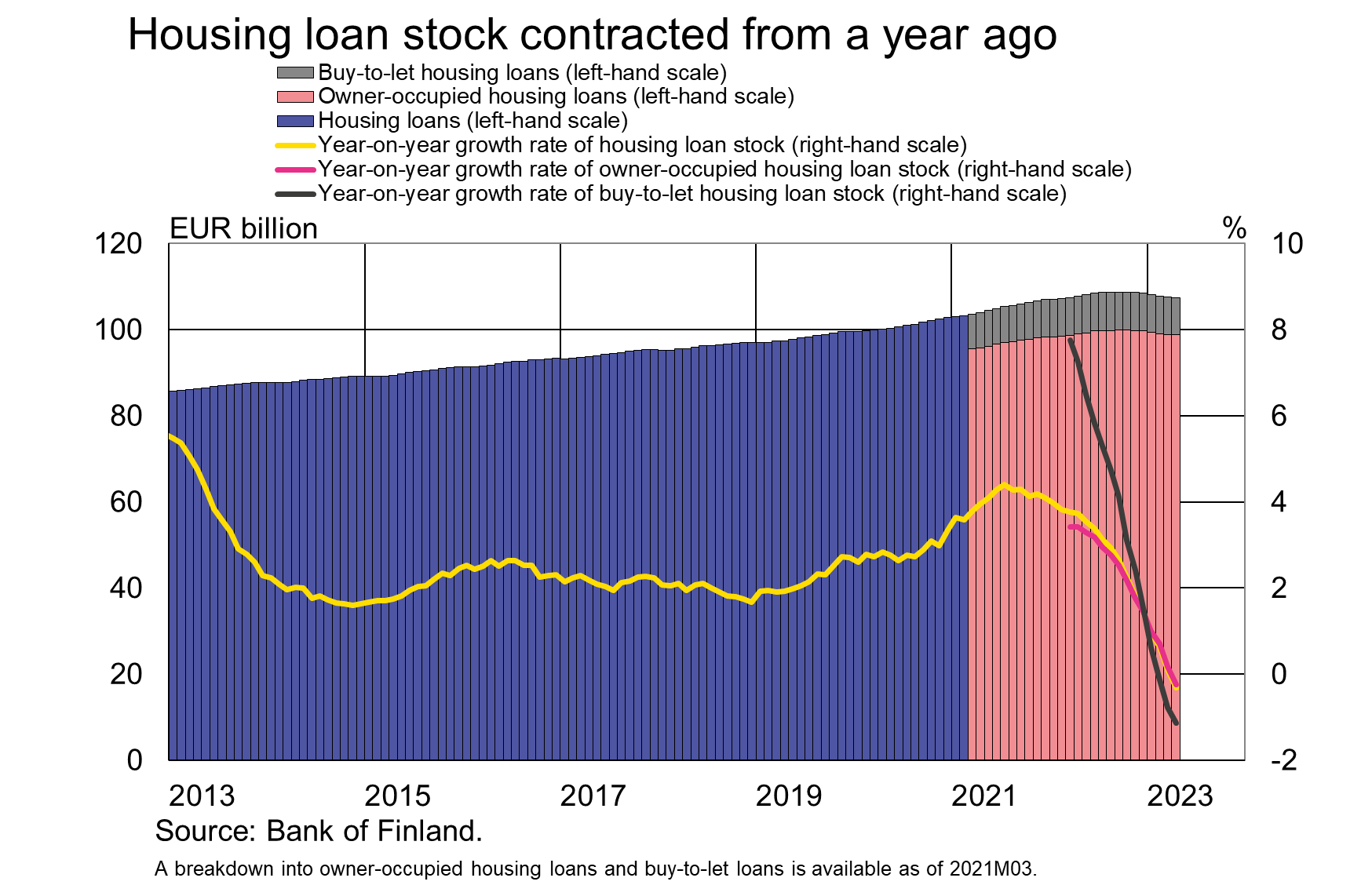

In April 2023, the stock of households’ housing loans exceptionally contracted by 0.3% year-on-year, having grown at an annual rate of 3.7% a year ago.

In April 2023, the stock of households’ housing loans exceptionally contracted by 0.3% year-on-year, having grown at an annual rate of 3.7% a year ago. The rate of growth of the buy-to-let housing loan stock has slowed down more abruptly during the year. In April 2023, the stock of buy-to-let housing loans (EUR 8.7 billion) contracted by 1.1% year-on-year, having grown at an annual rate of 7.3% at the same time a year earlier. At the same time, the stock of owner-occupied housing loans (EUR 98.7 billion) contracted by 0.3%, as opposed to a growth rate of 3.4% in April 2022.

The growth of the housing loan stock has been slowed down by a lower-than-usual drawdowns of housing loans. In April 2023, households drew down EUR 1.0 billion of new housing loans, which is 39% less than a year earlier. The last time drawdowns of housing loans were this low was 21 years ago, in 2002. In April 2023, EUR 950 million of the new housing loans were owner-occupied housing loans. The rise in interest rates on both owner-occupied and buy-to-let housing loans continued in April. The average interest rate on new corporate loan drawdowns rose by 0.2 percentage points from March, to 4.1%. At the same time, the average interest rate on new buy-to-let housing loans was 4.35% in April, or 0.17 percentage points higher than in March.

Higher interest rates are carried over to the housing loan stock with a delay reflecting the interest rate adjustment of floating rate loans. The rise of the average interest rate on the housing loan stock[1] is also slowed down by interest rate hedges taken out on the loans. In April 2023, the average interest rate on the housing loan stock was 2.86%, or 2.06 percentage points higher than at the same time last year. The average interest rate on the stock of buy-to-let housing loans (3.06%) has risen somewhat more during the year, i.e. 2.13 percentage points. Despite the rise in interest rates, the non-performing housing loan stock has not started to grow. Relative to the loan stock, the proportion of non-performing owner-occupied housing loans was higher (1.4%) than that of buy-to-let housing loans (0.9%).

Loans

At the end of April, Finnish households’ loan stock comprised EUR 16.9 billion in consumer credit and EUR 18.0 billion in other loans.

Drawdowns of new loans[2] by Finnish non-financial corporations amounted to EUR 1.8 billion, with loans to housing corporations’ loans accounting for EUR 490 million. The average interest rate on new corporate loan drawdowns rose from March, to stand at 4.95%. At the end of April, the stock of loans granted to Finnish non-financial corporations stood at EUR 105.3 billion, whereof loans to housing corporations accounted for EUR 43.1 billion.

Deposits

At the end of April 2023, the aggregate stock of Finnish households’ deposits totalled EUR 111.3 billion, and the average interest rate on these deposits was 0.51%. Overnight deposits accounted for EUR 99.6 billion and deposits with agreed maturity for EUR 6.5 billion of the total deposit stock. In April, Finnish households made EUR 750 million of new deposit agreements with an agreed maturity, at an average interest rate of 2.52%.

| Loans and deposits to Finland, preliminary data | |||||

| February, EUR million | March, EUR million | April, EUR million | April, 12-month change1, % | Average interest rate, % | |

| Loans to households, stock | 142,831 | 142,525 | 142,346 | -0.1 | 3.44 |

| - of which housing loans | 107,783 | 107,548 | 107,423 | -0.3 | 2.88 |

| - of which buy-to-let mortgages | 8,715 | 8,690 | 8,676 | 3.06 | |

| Loans to non-financial corporations2, stock | 104,655 | 104,702 | 105,308 | 4.8 | 3.67 |

| Deposits by households, stock | 110,225 | 109,913 | 111,317 | -1.0 | 0.51 |

| Households' new drawdowns of housing loans | 979 | 1,216 | 1,039 | 4.13 | |

| - of which buy-to-let mortgages | 81 | 96 | 89 | 4.35 | |

* Includes loans and deposits in all currencies to residents in Finland. The statistical releases of the Bank of Finland up to January 2021, as well as those of the ECB, present loans and deposits in euro to euro area residents and also include non-profit institutions serving households. For these reasons, the figures in this table differ from those in the aforementioned releases.

1 Rate of change has been calculated from monthly differences in levels adjusted for classification and other revaluation changes.

2 Non-financial corporations also include housing corporations.

- Euro-denominated deposits and loans of euro area residents: stock, 12 month rate of change and average interest rate

- Euro-denominated loans and deposits of Finnish households

- New business on loans and new drawdowns of household loans

- Finnish contribution to the euro area monetary aggregates and their main counterparts

- Imputed interest rate margins on loans from MFIs

For further information, please contact:

Antti Hirvonen, tel. +358 9 183 2121, email: antti.hirvonen(at)bof.fi,

Markus Aaltonen, tel. +358 9 183 2395, email: markus.aaltonen(at)bof.fi.

The next news release on money and banking statistics will be published at 10:00 on 29 June 2023.

Related statistical data and ‑graphs are also available on the Bank of Finland website at https://www.suomenpankki.fi/en/Statistics/mfi-balance-sheet/.

[1] The average interest on the housing loan stock indicates the interest rate paid by mortgage borrowers on average on their housing loans.

[2] Excl. overdrafts and credit card credit.