Housing loan drawdowns in July higher than normal

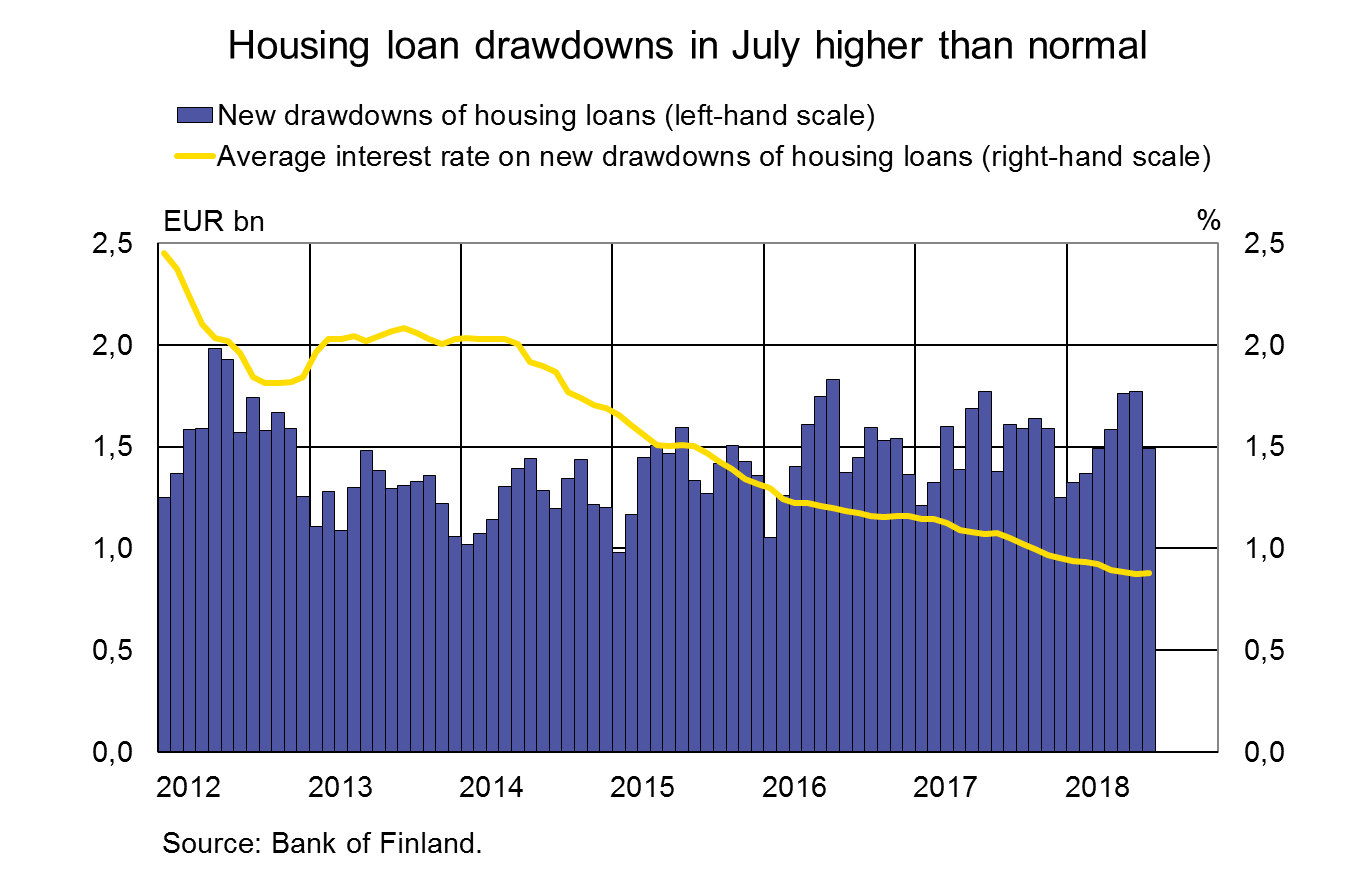

In July 2018, new drawdowns of housing loans amounted to EUR 1.5 bn, which is EUR 100 million more than in the corresponding period a year earlier. Housing loan drawdowns have last been higher in July in 2012. In January–July 2018, housing loan drawdowns were 4% higher than in the year-earlier period.

The annualised agreed rate on new housing loans rose slightly from June, to 0.88% in July 2018. The imputed margin1 was unchanged from June, at 0.85%. The imputed margin has decreased since 2013 and has last been lower in 2011.

The average repayment period of housing loans drawn down in July 2018 was 20 years, i.e. six months longer than in the year-earlier period. Over 60% of new housing loan drawdowns had a repayment period of 20–26 years in July. Housing loans with even longer repayment periods have become slightly more common during 2018, even though their share is still small. In July, 3% of housing loans had a repayment period of over 26 years.

Loans

Loans

At the end of July 2018, the stock of euro-denominated housing loans amounted to EUR 97.1 bn and the annual growth rate of the stock was 2.1%. Household credit at end-July comprised EUR 15.7 bn in consumer credit and EUR 16.8 bn in other loans.

New drawdowns of loans to non-financial corporations (excl. overdrafts and credit card credit) amounted to EUR 1.6 bn in July. The average interest rate on new corporate-loan drawdowns rose from June, to 2.18%. The stock of euro-denominated loans to non-financial corporations at end-July was EUR 83.0 bn, of which loans to housing corporations accounted for EUR 30.2 bn.

Deposits

At the end of July , the stock of household deposits totalled EUR 86.6 bn and the average interest rate on the deposits was 0.12%. Overnight deposits accounted for EUR 73.0 bn and deposits with agreed maturity for EUR 5.9 bn of the deposit stock. In July, households concluded EUR 0.2 bn of new agreements on deposits with agreed maturity, at an average interest rate of 0.30%.

1 Data on imputed margin has not been deducted by costs from interest rate hedges which affect the annualised agreed rate. According to the Bank of Finland estimate, costs from interest rate hedges for housing loans currently raise the imputed margin by 0.1–0.2 percentage point.

Key figures of Finnish MFIs' loans and deposits, preliminary data

| May, EUR million | June, EUR million | July, EUR million | July, 12-month change1, % | Average interest rate, % | |

| Loans to households2, stock | 128,981 | 129,555 | 129,648 | 2,5 | 1,49 |

| - of which housing loans | 96,698 | 97,080 | 97,111 | 2,1 | 0,98 |

| Loans to non-financial corporations2, stock | 81,863 | 83,112 | 83,020 | 6,4 | 1,38 |

| Deposits by households2, stock | 89,667 | 91,108 | 90,554 | 4,3 | 0,12 |

| Households' new drawdowns of housing loans | 1,762 | 1,770 | 1,493 | 0,88 |

1 Rate of change has been calculated from monthly differences in levels adjusted for classification and other revaluation changes.

2 Households also include non-profit institutions serving households; non-financial corporations also include housing corporations

- Euro-denominated deposits and loans of euro area residents: stock, 12 month rate of change and average interest rate

- Euro-denominated loans and deposits of Finnish households

- New business on loans and new drawdowns of household loans

- Finnish contribution to the euro area monetary aggregates and their main counterparts

- Imputed interest rate margins on loans from MFIs

For further information, please contact:

Markus Aaltonen, tel. +358 9 183 2395, email: markus.aaltonen(at)bof.fi

Ville Tolkki, tel. +358 9 183 2420, email: ville.tolkki(at)bof.fi.

The next news release will be published at 1 pm on 28 September 2018.

Related statistical data and graphs are also available on the Bank of Finland website: https://www.suomenpankki.fi/en/Statistics/mfi-balance-sheet/.